Board of Trustees adopts resolutions on future pension plan

The new pension plan: status update

The process of deciding on the new pension plan recently took another step forward. During the first calendar quarter of this year, the Accountability Body issued a favourable opinion on the Board’s provisional resolutions for the new pension plan. This allowed the Board to confirm its resolutions in late-March, subject to two contingencies. Read on to find out more: what is the current status of the process, what contingencies remain, and how will you, as a member of the Pension Fund, be impacted by the decisions that are made?

Roadmap towards your new pension

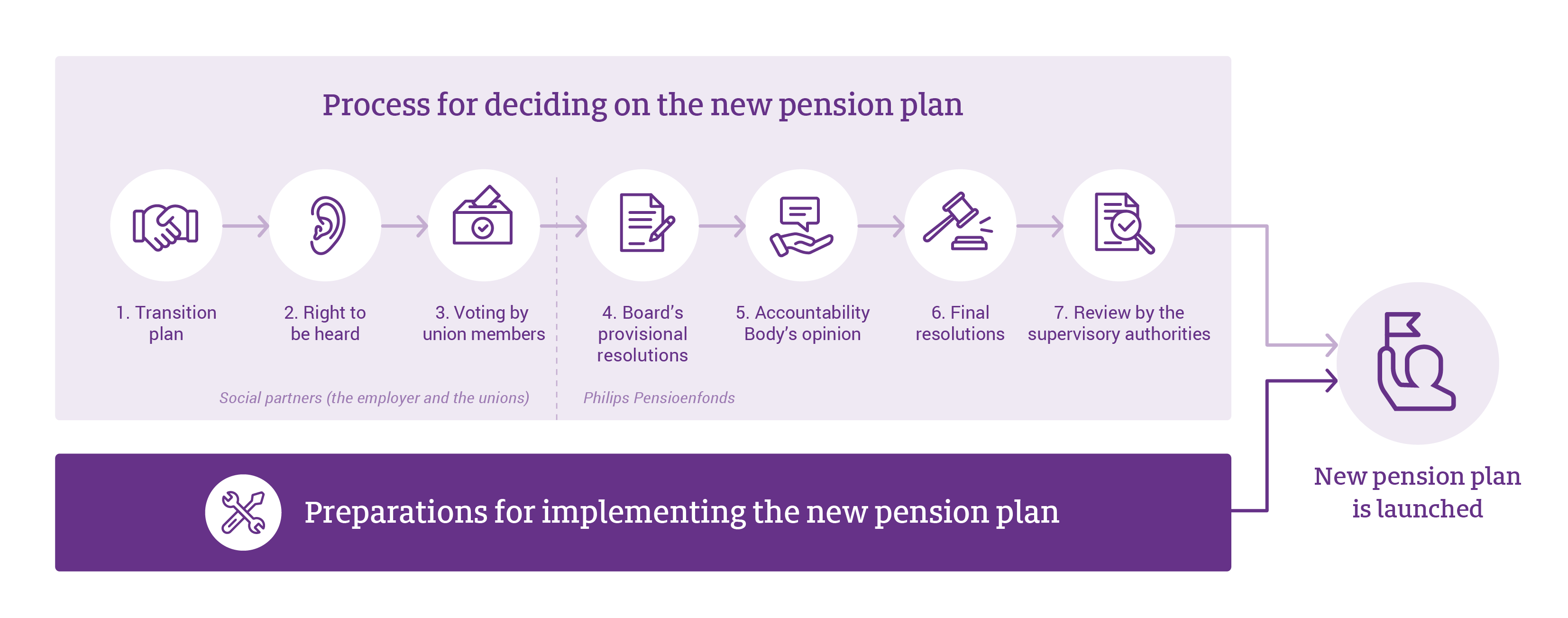

If everything proceeds according to plan, we will switch to the new pension plan on 1 January 2027. Before we make the final switch, various steps still have to be taken. Read on for a description of the entire decision process, or see the visual below for a summary.

What is the current status of the process?

In the December issue of our magazine Generaties, we announced that the social partners (i.e. employer and unions) had formalised the arrangements about the new pension plan in their transition plans. As part of that process, the Federatie van Philips Verenigingen van Gepensioneerden (FPVG, the federation of associations of Philips retirees) exercised its right to be heard. The FPVG gave its opinion on a pre-draft version of the transition plan, resulting in a couple of concrete changes in the finalised version. Although the changes work out to the benefit of our retired members, the social partners do not feel that they disturb the overall balance (See the Q&A section for details about the changes that were made). The finalised transition plans were adopted by the unions’ members in December, which completed Steps 1 to 3 of the process.

Provisional resolutions

Following this, the Board of Trustees adopted a series of provisional resolutions about the new pension plan (Step 4). This involved reviewing the transition plans adopted by the social partners, including the changes that were made after the FPVG exercised its right to be heard, as described above. The verdict was that the Board is willing to carry out the arrangements, in principle, based on how those arrangements will impact the various groups of members of Philips Pensioenfonds. In other words, the Board is of the opinion that the arrangements between the social partners are ‘balanced’. Before Philips Pensioenfonds can make a final decision about carrying out those arrangements, the technical feasibility of the pension plan needs to be determined, and the costs (Are they reasonable?) and risks (Can they be properly managed?) need to be studied. Find out more under ‘What contingencies remain?’.

Accountability Body’s opinion

Next, the Accountability Body was asked to give its opinion on various matters (Step 5). By law, the Accountability Body may give its opinion on the decision to convert the accrued pensions to the new pension plan (‘entitlement conversion’, or invaren in Dutch) and on how the Pension Fund’s assets are divided among the members’ personal pension capitals. In early-March, the Accountability Body issued a favourable opinion. It highlighted two matters in particular, which are explained in more detail below (see ‘How will you, as a member of the Pension Fund, be impacted by the decisions that are made?’):

- Under the new pension plan, it is unlikely that we will need to cut in the pensions that existing pension beneficiaries are currently drawing.

- Over the long term, the pensions are expected to go up by around 2% per year under the new pension plan.

‘Final’ resolutions

In late-March, following the Accountability Body’s favourable opinion, the Board confirmed its proposed resolutions. This represents a big step forward towards the new pension plan. The impact of those resolutions on our members was explained in our magazine Generaties. However, at this time we can provide more concrete details. See ‘How will you, as a member of the Pension Fund, be impacted by the decisions that are made?’.

What contingencies remain?

The previous paragraph explained that the resolutions are ‘final’. Those quotation marks are deliberate, since the resolutions are still subject to two contingencies:

- The implementation plan is not yet finalised: the implementation plan will be finalised by 1 July. This is a document that we have to submit to the Dutch central Bank (DNB) as our supervisory authority. We have to demonstrate that we are capable of implementing and administering the new pension plan, so the implementation plan needs to address the costs and risks, and how we intend to manage those risks. It also needs to explain the safeguards for data quality, and how the accrued pensions will be converted to the new pension plan. A last element that is mandatory to include in the implementation plan is a description of how we will communicate with our members about the switch to the new pension plan. That plan has to be presented to the Dutch Authority for the Financial Markets (AFM), our other supervisory authority.

- Approval from supervisory authority DNB: before we can convert the accrued pensions to the new pension plan, we need approval from DNB. We have to submit a large number of documents (including the implementation plan and a conversion template – the so called ‘invaarsjabloon’), which that supervisory authority will study before deciding whether it can grant its approval. Reviewing all those documents, a process that is referred to in practice as ‘reviewing the conversion request’, is labour-intensive, and we are working on the assumption that it will be 2026 before we know whether or not we have DNB’s approval.

Wat betekent de besluitvorming voor u als deelnemer?

How will you, as a member of the Pension Fund, be impacted by the decisions that are made?

In the ‘Did you know...?’ section in our magazine Generaties, we explained how the new pension plan will affect your future pension. The information presented there was based on the provisional resolutions. Now that the decisions have progressed another step forward, we can share more concrete details, by explaining how much higher your pension will be on 1 January 2027, assuming that our funding ratio remains strong. If the funding ratio is 120% when we switch to the new pension plan, we expect the effects to be as shown below. The advantages mentioned in the first two points of the list below will be smaller, of course, if the funding ratio is lower than 120% when we make the switch, and greater if it is higher. If the funding ratio drops below 115%, this will also negatively affect the degree of protection that the solidarity reserve can offer (See also the Q&A section at the bottom of this page).

- Immediately after we make the switch, every member will have a higher pension than under the existing pension plan. For our pension beneficiaries, it will be an increase of 5-8%.

- All our members are also expected to have a higher pension than under the existing pension plan over the entire period that they draw their pension.

- The so-called solidarity reserve provides pensions that are already being drawn with a high degree of protection against cuts. Pensions that have previously gone up are also strongly protected against cuts. The protection means that it will be less likely than under the existing pension plan that we have to lower the pensions that are being drawn.

- Measured over the long term, the pensions are expected to go up by an average of 2% per year. This means that the pensions are expected to retain at least most of their purchasing power.

This sounds very encouraging. Are there any risks?

Yes, of course this comes with some risks. Developments on the interest and stock markets are unpredictable, and investment yields could fall short of expectations. Inflation could be higher than we currently foresee, which would erode the pensions’ purchasing power over time. These risks already exist under the pension plan that we have now. Under the existing pension plan, the Pension Fund is required to maintain a buffer, which offers members protection in case the investment returns fall short. So how does this work under the new pension plan?

Risks for pension beneficiaries

In the new pension plan, pension beneficiaries of Philips Pensioenfonds are protected against shortfalls in investment returns by the solidarity reserve. At the time of switching to the new pension plan, that reserve will be filled using the Pension Fund’s buffer. Later, it will be topped up by withholding small amounts from the positive investment yields of the pension beneficiaries and other members aged 55 and up. The solidarity reserve will be used to top up your pension if it would otherwise need to be lowered. However, this is possible only if the solidarity reserve contains enough assets.

Risks for active members and non-contributory policyholders

The solidarity reserve does not protect active members and non-contributory policyholders before they start drawing their pension. The new pension plan will not include a financial buffer, meaning that negative investment returns will have a direct negative impact on the personal pension capital of those members, and on their expected pension. At the same time, however, positive investment returns will cause a direct increase in their expected pension. Under the existing system, positive investment yields are generally only used to increase the buffer, and so improve the funding ratio. A member’s pension (actual or expected) only goes up if the Pension Fund can award indexation (including compensatory indexation) on the pensions. This is explained in more detail below.

When to expect more information

We will bring a special issue of our magazine Generaties in the third calendar quarter of 2025. That special issue will be devoted entirely to the new pension plan, and will also cover more information about the Board’s resolutions. If you cannot wait until then, or if you would like more specific information, visit our website, where the full implementation plan and a summary of the communication plan will be posted on 1 July 2025.

Questions and answers

About the final resolutions

of the Board of Trustees

- Slightly more risk in the investment policy

As a result of this change, the average annual amount by which the pensions are expected to go up under the new pension plan is a little higher. - Shorter 3-year spread instead of a 5-year spread

Under the new pension plan, the investment yields will be spread over time. Your pension will not change immediately as a result of positive or negative returns on the investments. Instead, those returns will be spread over several years to give your pension greater stability. A shorter spread means that positive returns will have a more immediate positive effect on the pension benefits. At the same time, it is very unlikely that the pensions will need to be cut, thanks to the collective ‘solidarity reserve’ that will protect the pensions if the investment yields and other results fall short. - A technical adjustment to the calculation method

The transition plan explains what calculation method will be used to establish our members’ personal pension capital when we make the switch. Following a technical adjustment, the pension capitals of pension beneficiaries will be allocated a total of over € 86 million more than under the earlier method.

In the article above, we explained how the arrangements about the new pension plan are expected to impact your future pension, assuming a 120% funding ratio when we make the switch.

Policy of protecting the financial buffer

It is important to understand that the Pension Fund’s policy is to prevent, if at all possible, any drop in the funding ratio as a result of poor investment returns. Until we switch to the new pension plan, we will do this by investing in fixed-income securities and by hedging most of the interest risk. The funding ratio also goes down when we grant indexation. Indexation is granted by resolution of the Board of Trustees, though: every year, the Board of Trustees decides whether it is justified to index the pensions, bearing in mind how that would affect the Pension Fund’s funding ratio.

How the buffer will be shared when we switch to the new pension plan?

How high the funding ratio is, will have a direct impact on how much pension you will have after the switch. Under the new pension plan, the Pension Fund no longer has to maintain a financial buffer. However, there is the aforementioned solidarity reserve to pay compensation for shortfalls to members who are drawing a pension and a small amount for unforeseen expenditure. This will be set up using part of the financial buffer at the moment of the switch. But part of that buffer will be added directly to each member’s personal pension capital, and so immediately after the switch you will have more pension than under the existing pension plan. Of course this is possible only if the funding ratio does not drop significantly between now and when we make the switch. The transition plan includes a method for ‘sharing’ the buffer, so that all our members get off to a strong and balanced start under the new pension plan. Read the Q&A below to find out more about how this works.

See the news item above for an explanation of how the arrangements about the new pension plan are expected to impact your future pension, assuming a 120% funding ratio when we make the switch. If the funding ratio undergoes any significant downturn before the date of the switch, this will have an impact as described in the following points.

- If the funding ratio falls from its present level but remains above 115%, the resources are sufficient to compensate for abolishing the system of averaged contributions (click here for a Q&A about this topic). It will also be enough to top up the solidarity reserve to the initial level that we want, and the protection that the solidarity reserve offers will not be affected in this scenario. However, individual members will have less money in their personal pension capital, and this will impact the positive effects described above (the first two points under ‘What is your future pension expected to be?’)

- If the funding ratio drops below 115% and we are unable to top up the solidarity reserve to our preferred initial amount, this will negatively affect the degree of protection that the solidarity reserve can offer. The less is in it when we switch to the new pension plan, the less protection it will give, and the more likely it will be that pensions will need to be lowered. Of course the benefits described under the first two points under the heading ‘What is your future pension expected to be?’ will also be diminished if the funding ratio is less than 115%.

- If the funding ratio is less than 102% at the time of the conversion, the Pension Fund will consult with the social partners to discuss whether a balanced conversion (i.e. converting the pensions that have been accrued under the existing system to the new pension plan) will in fact be possible then. If the decision is made to proceed with the conversion, the compensation for abolishing the averaged contribution system will not be paid from the Pension Fund’s assets, but from the pension contributions.

It is important to understand that the Pension Fund’s policy is to prevent, if at all possible, any drop in the funding ratio as a result of poor investment returns. Until we switch to the new pension plan, we will do this by investing in fixed-income securities and by hedging most of the interest risk. The funding ratio also goes down when we grant indexation. Indexation is granted by resolution of the Board of Trustees, though: every year, the Board of Trustees decides whether it is justified to index the pensions, bearing in mind how that would affect the Pension Fund’s funding ratio.

The ‘allocation key’ or ‘conversion method’ reflects how the Pension Fund’s financial buffer will be shared among each member’s personal pension capital.

In the existing pension system, Philips Pensioenfonds has a realistic ambition: the Pension Fund wants full pension accrual and full indexation for all its members. The realistic ambition was the basis for deciding how to give shape to the new pension plan under the new system and the transition to that new pension plan.

The Pension Fund’s realistic ambition was also the basis for the decisions on the most balanced way of achieving this. With this ambition in mind, it is appropriate and fair to take into account both past indexation arrears and future indexation when allocating the buffer that has been built up under the existing pension system. Ignoring past indexation arrears would impact on older members in particular, while not considering future indexation would disadvantage younger members more.

For the allocation key in the transition plan of social partners of the employers, it is decided to adopt the ‘50/50’ method. With this method, indexation arrears carry as much weight as future indexation. To avoid confusion: 50/50 does not mean that the share of the Pension Fund’s assets that goes towards indexation arrears is the same as the share going to future indexation. So what does it mean? Each member’s personal pension capital will include an amount for financing a specific percentage (one that is the same for everyone) for the future indexation ambition, plus an amount for financing the same percentage of the indexation arrears (calculated in a uniform manner).

Financing indexation arrears is relatively more costly for older members, who have accrued more pension than younger members. Younger members, however, need relatively more money to realise future indexation than older members do: the future indexation for younger members needs to be financed over a longer time.

The allocation key described in the transition plan does not literally cover everyone’s missed indexation. Instead, it is decided to grant each member a uniform increase, that could be considered to be compensation for indexation that they missed in the past.

To do this, a uniform indexation arrear will be used. That uniform indexation arrear is based on the maximum indexation arrears among pension beneficiaries as published in the Pension Fund’s 2023 annual report, which works out at 16.1% missed indexation. The principal reason why is decided on a uniform indexation arrear is that this approach is both simple and easy to explain.

In practice, many of our members have less of an indexation arrear than the arrears described in the Pension Fund’s annual report. Each member’s indexation arrear is determined by when their employment began, how much indexation they were awarded and how much pension they accrued during their years of employment and how their salary increased, and so the actual indexation arrears varies strongly from one member to the next. It would need to be calculated and explained at the level of each individual and would become very complicated. It is not aimed to give everyone a precise percentage of their arrears, but rather a total sum that covers both the fact that money is needed to retain the future purchasing power of accrued rights and the fact that there are indexation arrears.